8 August, 2022 - Markets continue to move at incredible speeds.

- Konstantinos Tzavras, CIO

- Aug 8, 2022

- 6 min read

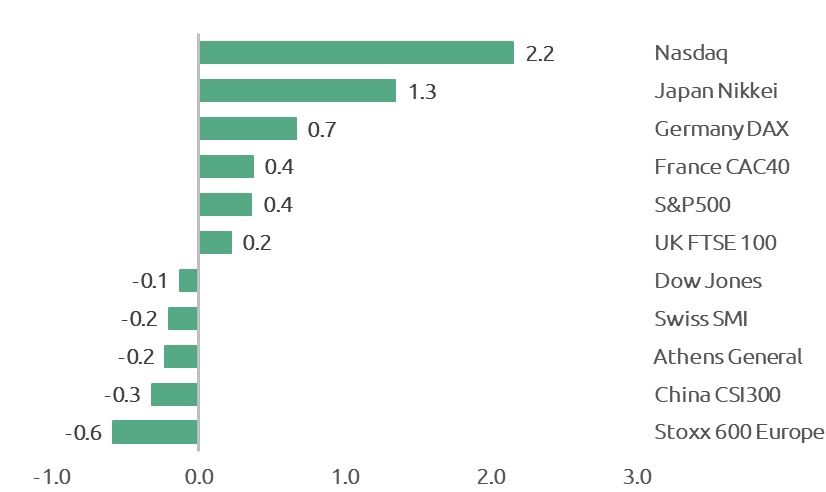

The expected "summer rally" has at last realized, but at a speed which perhaps makers it already mature and prone for a correction. After a horrible June, July offered significant gains to equity investors. The S&P500 rose by almost 9%, while Nasdaq gained more than 12%. Nasdaq is now almost 20% higher from its low, which was registered only in late June. Europe gained "only" 5% in the same period, as investors continue to fear a tough winter ahead for the region. However, parts of the European markets, such as Technology and Consumer Discretionary rallied by more than 10%. In contrast, China lost ground in July, with the MSCI China index down about 5%. But one should keep in mind, that the Chinese markets were rallying in June as the rest of the global equities were slumping. All in all, the speed and the extent of the rally, especially in US equities, makes us cautious again and a reduction of risk at these levels could perhaps be a good idea.

"Peak hawkishness" was the theme and the excuse for the July rally. All major Central Banks raised interest rates aggressively in the past two weeks, but at the same time there were more signs that the worst could be over with respect to inflation. Hence the markets were quick to jump to the conclusion that we are probably close to the peak of interest rate hikes and that central bankers will become less "hawkish" (i.e. with less desire to raise rates) after the upcoming September meetings. An indication of this scenario, is the maximum expected FED rate level of this cycle, as this is priced by the bond market. It had reached 4.30% just two months ago, and it now stands at 3.30%. However, the hot jobs report (see further below) might change this theme again. Already after the report, the market just priced in a 75bps hike in September, although a 50bps was becoming a consensus.

The July CPI (inflation) number in the US is out this week. The headline number is expected to show some slowdown on an annual basis, to 8.7% down from 9.1% in June. The Core CPI (which excludes food & energy) is expected to remain around 6%.

The ECB raised interest rates by 50bps to end the negative rates regime after several years, and the Governing Council (GC) approved the new Transmission Protection Instrument which would enable the ECB, at the GC's discretion, to selectively intervene in secondary bond markets to counter "unwarranted, disorderly market dynamics that pose a serious threat to the transmission of monetary policy across the euro area". This basically refers to protecting Italy and the rest of the periphery and was taken positively by the markets.

The FED raised rates again by 75bps, to a new range of 2.25%-2.50%. FED officials continued their rhetoric on the need to fight inflation almost at any cost, and another 75bps in September cannot be ruled out. This increase will take the FED rate to 3.00%-3.25%, at which point the FED could take the foot off the accelerator. It will need to asses the"damage" to the economy and/or to inflation by October, for its next moves. The Bank of England raised rates by 50bps, for the first time since 1995, to bring its own main rates to 1.75%.

The US economy is now in "technical recession", according to the definition of two consecutive quarters of negative GDP growth. The 2nd quarter GDP number was published at -0.9%, vs expectations for a rise by 0.8%. This follows the -1.6% of the 1st quarter GDP. However, an official recession is declared by a committee at the National Bureau of Economic Research (NBER), and we will have to wait. With unemployment at 3.5% and many economic indicators such as the PMI indices still in expansion territory (ie above 50), it certainly does not feel like a real recession (yet).

The US July ISM Manufacturing index, however, dropped to the lowest level in two years, at 52.8. More worrying was the New Orders component which dropped below 50 to 48.0, and this shows a high probability of a recession down the road. On a more "positive" side, the Prices Paid component fell by a whopping 18 points, which means that inflationary pressures seem to be easing.

But the US labor market continues to shine. The July non-farm payrolls were announced at +528'000 vs expectations of +250'000 and the unemployment fell to 3.5%. A major part of the strong number was a big increase in leisure related jobs, as the travel and hospitality industry this year is having an "out-of-this-world" moment due to the desire of individuals to move around and go out after two years of pandemic restrictions. But even if one accounts for that, the labor market remains hot, or "too hot" as the FED's Chairman called it. This number might change again the market's perception about when and where the FED will stop raising interest rates.

Gold managed to stage a rebound from below 1700$ to make an attempt again towards 1800$. The 1675/80$ levels, which were also the low of 2021, provided support to the yellow metal, for now. What is interesting is that this rebound is taking place at a time when the rest of the commodity complex (Energy, Food and Metals) are finding themselves in a bear market, falling 25%-30% from their peaks in June. It is interesting to see if Gold can keep this momentum, if the rest of the commodities continue to move lower.

Government bond yields fell to the lowest level since March, despite the rise on Friday after the unemployment report. The US 10-year yield closed at 2.80%, while the German equivalent at 0.95%, jumping 10bps on Friday.

Equities: Weekly Performances

Charts of the Week

US Government bonds started discounting the next recession

The yield on the 5-year US Treasury bond has fallen from the high of 3.50% in mid-June to about 2.85% in less than two months. This 65bps drop in yield translates to about 3.5% gains in price, making our call back in June to invest in this category of bonds, already profitable. The reason for this fall in yield (rise in price) is exactly what we were expecting to happen: given the aggressive increase of short-term interest rates by the FED and the various geopolitical issues globally, an economic recession in the coming months cannot be ruled out. If a recession hits, then the FED will stop raising rates and will probably engage in the next cycle of lowering rates again. The best vehicle for discounting this scenario is the 3-5 year maturities of government or very high quality bonds, for which we still maintain our recent positive view.

August could be a tricky month for equities

This (hard to read) but interesting chart shows the seasonal trends of August for the S&P500 index. The highlighted rectangle shows the average performance of August when the index is already down since the beginning of the year more than 5%, which is the case in 2022 too. The average August performance is a negative 1.6%. Even more worrying is the second column in the same rectangle (light pink), which shows the average performance after August until the end of the year, which is a negative 12.5%, with an average yearly drop of 25%. Of course these are just statistical observations and they are just averages, which means various outcomes are possible. However, as equity markets have moved very quickly up to significant resistance levels in July, one could argue that August might not be similarly kind to investors. Caution is warranted and purchases in 2022 are better to be made on weakness and not after big rallies.

Disclaimer

• The content of this document has been produced from publicly available information as well as from internal research and rigorous efforts have been made to verify the accuracy and reasonableness of the hypotheses used. Although unlikely, omissions or errors might however happen.

• The data included in this document are based on past performances and do not constitute an indicator or a guarantee of future performances. Performances are not constant over time and can be positive or negative.

• This document is intended for informational purposes only and should not be construed as an offer or solicitation for the purchase or sale of any financial instrument and it should not be considered as investment advice. The market valuations, views, and calculations contained herein are estimates only and are subject to change without notice. Any investment decision needs to be discussed with your advisor and cannot be based only on this document.

• This document is strictly confidential and should not be distributed further without the explicit consent of Kendra Securities House SA.

• Sources: Equity performace: Factshet, Chart 1: Factset, Chart 2: Pictet

Comments